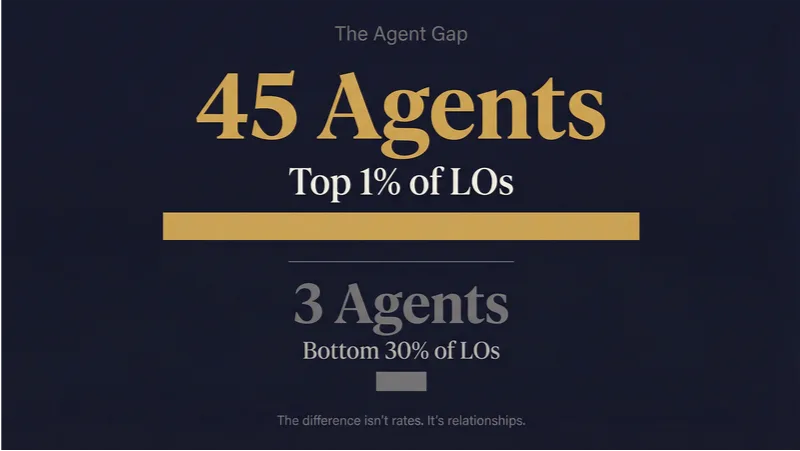

The top 1% of loan officers work with at least 45 real estate agents. The bottom 30% work with three or fewer. That gap tells you almost everything you need to know about why some LOs have a full pipeline and others are wondering where the referrals went.

Most loan officers think they’re doing enough to earn agent referrals. They buy the occasional coffee, drop off rate sheets, and wait for the phone to ring. But the numbers tell a different story about what actually works in mortgage referral strategy.

This is the uncomfortable truth: most LOs treat relationships as transactional lead sources rather than partnerships worth investing in. The ones who consistently win referral business are doing something their competitors dismiss as old-fashioned. They’re showing up personally and staying visible between transactions.

The Referral Economy Is the Whole Economy

Mike DelPrete’s analysis from February 2025 puts the numbers in stark relief: 87% of mortgage business comes from referrals and past clients. STRATMOR Group data shows 60-67% of mortgage transactions originate from the LO’s referral network. This isn’t one channel among many. It’s the business.

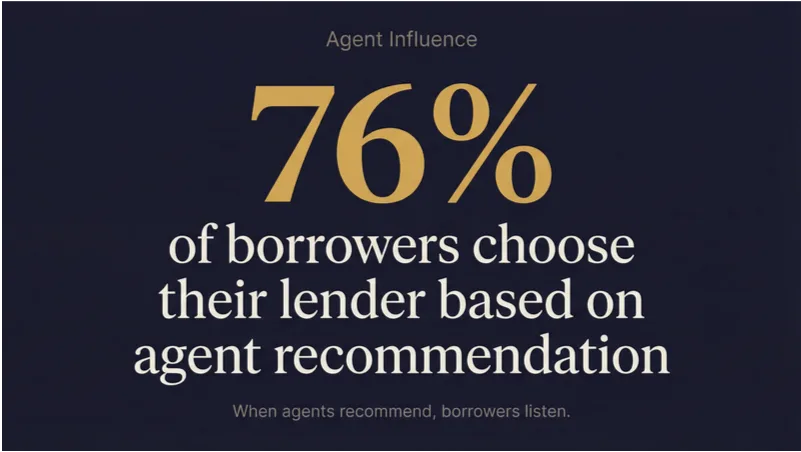

The agent’s role in this ecosystem is hard to overstate. According to Freddie Mac research, 76% of borrowers choose their mortgage provider based on their real estate agent’s recommendation. The National Association of Realtors reports that 88% of home purchases happen through an agent or broker. When agents recommend lenders, borrowers listen.

The data from Mobility Market Intelligence breaks down the gap by production tier. The top 1% of loan officers (the “Unicorn Tier”) work with at least 45 buy-side agents. The Diamond Tier (next 4%) works with 26. Platinum (next 15%) works with 14. Gold (next 20%) works with 7. And the Silver Tier, the bottom 30%, works with 3 or fewer. The difference between tiers isn’t product menu or rate competitiveness. It’s relationship depth and breadth.

Yet at large brokerages with in-house mortgage divisions, it’s common for only about a third of agents to consistently refer business to the affiliated lender. The rest default to outside LOs they have personal relationships with. The brokerage pays to maintain the lending division. The agents ignore it. The disconnect is almost always relational, not financial.

What Top Producers Actually Do Differently

STRATMOR Group’s MortgageCX program collects borrower feedback from tens of thousands of transactions. The data reveals what behaviors actually earn referrals, and it has nothing to do with rate sheets.

Top-producing LOs translate complexity into plain language. They don’t talk about LTV ratios. They explain what percentage of the home the loan will cover. They don’t mention DTI. They compare monthly payments to income in terms that make sense to someone who doesn’t live in mortgage software.

They communicate proactively and often. They set expectations at application about when and how they’ll touch base. They don’t wait for borrowers to ask for updates. They own mistakes instead of blaming underwriters, processors, or the system.

Most critically, they invest in the relationship when there’s no transaction on the table. The average homebuyer transacts once every 7-10 years. If you only show up during active deals, you’re absent for 95% of the relationship. The LOs who win referral business are the ones who stay visible when there’s no commission at stake.

Why Digital-Only Outreach Fails

The loan officers struggling to build agent networks often rely heavily on digital touchpoints. Email drip campaigns. CRM sequences. Social media posts. The problem isn’t that these tools are useless. It’s that they’re invisible.

Industry benchmarks show real estate email open rates sit around one in five. That means the vast majority of messages never get read. Agents can tell when they’re in an automated sequence. They know the difference between a templated check-in and something written for them.

The LOs who rely exclusively on digital touchpoints become invisible between closings. They’re out of sight for the 6-18 months that pass between transactions, then surprised when agents don’t remember them when the next referral opportunity comes up.

The Between-Transaction Gap

This is where most loan officer agent relationships die: the silence between deals. You close a transaction together, the borrower gets their keys, everyone celebrates, and then you disappear for a year. When that agent has their next referral, you’re competing with the LO who sent them a handwritten note last month, who dropped by their open house, who checked in after their vacation.

Staying top-of-mind requires physical, personal touchpoints. Handwritten notes, face-to-face drop-ins, personal check-ins that aren’t about business. The data on physical mail effectiveness makes the case clearly: direct mail generates 37x higher response rates than email, and handwritten envelopes achieve 99% open rates. Services like Stylograph capture a person’s actual handwriting and apply it to personalized notes at scale, so the outreach stays genuine without consuming your calendar. We broke down the exact ROI math on handwritten outreach for mortgage referrals in our companion post.

For deeper context on the broader agent-LO relationship ecosystem, explore how client retention strategies apply to real estate agents and why in-house lending referral rates remain low.

The point isn’t to automate your relationships. It’s to scale the personal touches that actually build trust without requiring impossible amounts of your time.

The Consolidation Multiplier

The mortgage industry has been consolidating. According to RETR data reported by HousingWire, the LO population dropped 43% from its 2021 peak to early 2024. Real estate agent counts fell another 3% in 2025 to 1,055,912.

Fewer agents and fewer LOs means each surviving relationship carries disproportionate weight. RETR co-founder Steven Wynands put it directly: “This is a time to stick around and double down on relationships, because it’s when things get better.”

Investing in agent relationships now, while competitors are cutting costs and going quiet, creates a moat that’s hard to replicate when the market recovers. The LOs who stay visible during the down cycle will own the referral relationships when volume returns.

What This Means for Your Referral Strategy

The MMI tier data is uncomfortable because it’s specific. You know exactly where you fall. If you’re working with three agents and the top performers are working with forty-five, the gap isn’t luck or timing. It’s strategy.

The good news: relationship depth is something you can start building today. It starts with a decision to invest in visibility between transactions, not just performance during them. The LOs who do this consistently are the ones who win the referrals when agents make those recommendations that drive 76% of borrower decisions.

FAQ

How do loan officers get more referrals from real estate agents?

Research from Mike DelPrete and STRATMOR Group shows 87% of mortgage business comes from referrals and past clients. The loan officers who earn the most referrals invest in personal relationships with agents through consistent communication, plain-language explanations, and staying visible between transactions. Top-producing LOs work with 45+ agents while bottom performers work with 3 or fewer. The gap comes down to relationship investment, not rate competitiveness.

Why don’t agents refer to in-house mortgage lenders?

At brokerages with in-house mortgage divisions, the gap between expectation and reality usually comes down to relationships. Outside loan officers who invest in personal connections often win referrals over affiliated lenders because they’ve built trust through consistent, personal communication between transactions.

What is the best way for loan officers to stay top of mind with agents?

Staying top-of-mind requires physical, personal touchpoints during the 6-18 months between transactions. Handwritten notes, face-to-face drop-ins, and personal check-ins that aren’t about business are most effective. Digital-only approaches fall short because email open rates in real estate sit around one in five, and agents can tell when they’re in an automated sequence.