Most real estate agents don’t refer buyers to their brokerage’s affiliated lender. Not because the rates are wrong. Not because the products are inferior. They don’t refer because they don’t have a personal relationship with the loan officer down the hall. The lending division and the sales floor operate as separate worlds, with no systematic touchpoint connecting the two. It is not a pricing problem or a product problem. It is an invisibility problem.

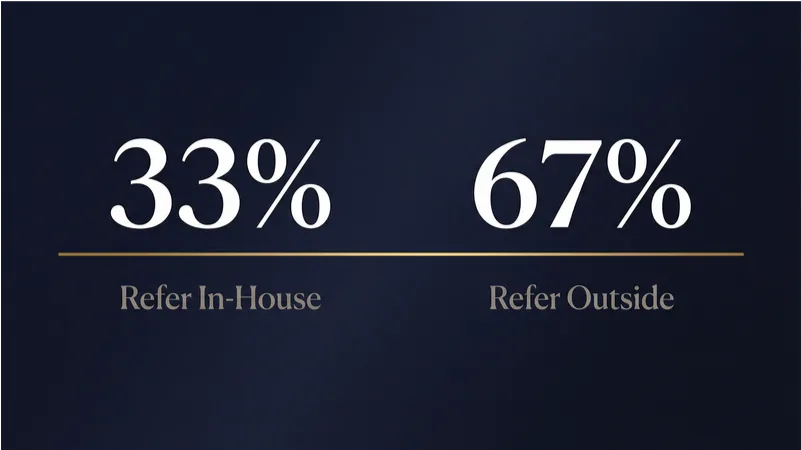

One-Third Refer. Two-Thirds Walk.

At a top-10 U.S. brokerage with an in-house mortgage division and more than 10,000 agents, roughly one-third consistently refer their buyers to the affiliated lender. The other two-thirds send those buyers to outside banks, credit unions, or independent mortgage brokers they already know from past transactions.

Think about what that means in revenue terms. If 6,500 agents are each closing a handful of transactions per year and referring every buyer externally, that is thousands of mortgage originations leaving the brokerage ecosystem annually. At average origination revenue, the unrealized income reaches into the tens of millions. This is not a rounding error. It shows up on the P&L.

A Freddie Mac survey of licensed real estate professionals found that 76% say their clients “always or often” use their recommended lender. So agents have enormous influence over where buyers get their mortgage. The question is not whether agents drive lending decisions. The question is why those referrals flow outside the building instead of across it.

Why It Happens

The Org Chart Problem

The lending division and the sales floor live under the same brand, but they operate as separate business units. Different managers. Different profit-and-loss statements. Different incentive structures. When a new loan officer joins the affiliated lender, they do not get introduced to the 200 agents in their territory. There is no onboarding moment where someone says, “Here is your lending counterpart. You two should talk.”

This structural gap means that relationship-building between the two sides is left entirely to individual initiative. Some loan officers are proactive enough to bridge it. Most are not.

The Relationship Default

Agents refer to lenders they trust. That trust was built through years of closed transactions, responsive communication during stressful moments, and smooth closings that made the agent look good to their client. An affiliated lender cannot compete with that kind of history by sending a rate sheet.

When agents are asked why they don’t refer internally, the answer is rarely about pricing. It is almost always some version of: “I already have a lender I trust.”

The data backs this up. A STRATMOR Group study reported by Inman in February 2025 surveyed 82,000 recent homebuyers and found that 87% found their mortgage lender through either a personal referral (50%) or an existing lending relationship (37%). Mortgage is a relationship-driven business from the borrower’s perspective, too. If the affiliated lender has not built a relationship with the agent, they are effectively invisible to the buyer.

The First-Touch Gap

When a new lead comes in from a website inquiry or open house, the agent gets notified. The loan officer in that region may also get notified. Both are expected to act on the lead independently. But the loan officer has no mechanism to introduce themselves to the buyer in a way that feels personal and trustworthy before the agent has already recommended their usual outside lender.

By the time the affiliated lender reaches out, the decision has already been made. The loan officer is not competing on rates at that point. They never got the chance to compete at all.

What Doesn’t Work

Brokerages have tried to solve this problem through scale. The approaches are familiar:

Rate sheets and email campaigns. Loan officers send agents weekly rate updates. Agents ignore them. Rates are a commodity, and every lender in town has competitive pricing.

Lunch-and-learns. Loan officers host educational sessions for agents. Attendance is thin because agents are busy showing houses and writing offers. The agents who do attend are usually the ones already referring internally.

CRM drip sequences. Automated emails from the lending division land in agent inboxes and get deleted unread. The messages are generic, impersonal, and indistinguishable from the hundred other automated emails agents receive each week. It is the same dynamic driving AI fatigue across marketing more broadly: when everything is automated, nothing feels personal.

The common thread: all of these approaches optimize for reach rather than depth. They assume the problem is awareness. It is not. Agents know the affiliated lender exists. What they lack is a personal connection to a specific loan officer they believe will take care of their client.

MGIC’s 2024 Loan Originators Survey confirms this. Eighty-six percent of loan officers say excellent and responsive service is the most important factor in earning agent referrals. The gap is not information. It is the frequency and quality of personal contact.

What Actually Works

The referral problem gets solved at the individual relationship level, not the organizational level. Brokerage-wide mandates and top-down directives do not change agent behavior. What changes behavior is giving individual loan officers the tools and habits to build personal connections with agents, one relationship at a time.

Three approaches consistently move the number:

Systematic Personal Outreach

Loan officers who maintain weekly personal touchpoints with their top agent prospects consistently outperform those who rely on marketing campaigns. The medium matters less than the consistency and the personalization. A brief, specific handwritten note referencing a recent listing or a closed deal signals attention that a mass email never will. The research on handwritten mail response rates quantifies the gap: direct mail delivers 37x higher response rates than email, and handwritten envelopes hit 99% open rates versus roughly 20% for digital outreach.

For practical examples of personal outreach ROI at scale, see our analysis of how handwritten notes drive mortgage referral revenue, and for agents looking to strengthen their own client relationships, explore client retention and repeat business strategies.

This is where technology can help. Tools like Stylograph allow loan officers to send personalized, handwritten notes at scale, combining the authenticity of a personal touch with the consistency of a systematic outreach program. The key is staying on the right side of the authenticity line: technology should amplify a real person’s effort, not simulate it.

First-Touch Acceleration

Getting the loan officer in front of the buyer early, ideally within 48 hours of a new lead, before the agent makes a referral decision. The mechanism can vary: a phone call, a handwritten welcome note, a text message. The goal is the same in every case. Make the loan officer a real person to the buyer before they become a name buried in a rate comparison spreadsheet.

Closing the Loop

Loan officers who proactively update the referring agent throughout the lending process build trust that compounds across transactions. A quick call or note when the application is received, when the appraisal is scheduled, or when the file reaches clear-to-close signals reliability. STRATMOR Group research recommends that loan officers make personal contact with their top referral partners at least once per week.

Over time, these touchpoints transform a transactional handoff into a working partnership. The agent starts to view that loan officer as “their lender,” and the referrals follow.

The Compound Effect

When a loan officer converts even a handful of non-referring agents into regular referral partners, the math compounds quickly. Each new agent relationship is not a single transaction. It is a pipeline. One agent closing 8-12 buy-side transactions per year represents a steady stream of mortgage originations for years to come.

At the brokerage level, moving the referral rate from 33% to 40% does not require a revolution. It does not require convincing every agent. It requires equipping loan officers with the right tools and touchpoints to build relationships with the agents who are reachable but not yet connected.

For a large brokerage, that 7-point shift represents a meaningful revenue gain. And it starts with the simplest thing in business: one person reaching out to another in a way that feels personal, specific, and real.

FAQ

How do you increase mortgage referrals from real estate agents?

Build a personal relationship with each agent through consistent, personalized outreach. The most effective loan officers maintain weekly contact with their top agent prospects and provide proactive updates on every shared transaction. Rate sheets, email blasts, and company mandates do not move the needle. Relationships do.

Why do real estate agents refer to outside lenders instead of in-house?

Agents refer to lenders they already trust from past transactions. Affiliated lenders often fail to build those personal relationships because the lending and sales divisions operate as separate business units with no structured connection points. The problem is not rates or product offerings. It is relationship proximity.